And it’s structural. Variable-rate CRE mortgages and much higher rates just speed up the process.

By Wolf Richter for WOLF STREET.

Office mortgages that had been packaged into CMBS went through a horrendous default cycle following the Financial Crisis, with the delinquency rate topping out at over 10% in 2012/2013.

But this current six-month 2.9-percentage-point spike from 1.6% to 4.5% is the fastest six-month spike in Trepp’s data going back to 2000.

So this is going to be interesting because we’re just at the beginning of a massive structural change – not a temporary blip – that is impacting office towers; turns out, companies have figured out they won’t ever need this vast amount of vacant office space.

Trepp considers a loan “delinquent” after the penalty-free 30-day grace period ends and the borrower still hasn’t caught up with the interest payment.

This delinquency rate does not include properties that are still paying interest but are past due on paying off the mortgage on maturity date. This includes the interest-only mortgages, when the whole amount is due at maturity, and mortgages with a balloon payment at maturity. As long as landlords are making interest payments, Trepp doesn’t consider the mortgages delinquent, but tracks mortgages that are past their maturity date separately.

For example, Trepp’s overall delinquency rate for all types of CMBS rose to 3.90% in June. Including the loans that were past their maturity date but were still paying interest, the delinquency rate would have risen to 4.66%.

CMBS have real advantages. They allow lenders, such as banks, to sell high-risk commercial mortgages during times of low interest rates to yield-chasing investors, such as bond funds, life insurers, etc. For banks, these mortgages might be too risky to keep on their books.

So they package them, sometimes just one big mortgage, but often several or many mortgages, into a pool of mortgages that then gets structured into different slices that investors buy, with the junk-rated slices taking the first losses in return for slightly higher yields. The top-rated slices have an A-rating or AA-rating, solidly investment grade (here’s my cheat sheet on bond credit ratings by rating agency), with the idea that the lowest rated slices will absorb any losses while the top-rated slices remain unscathed.

The mortgages – as we have seen in the current wave of defaults, including those where the landlord has just walked away from the property – are often variable-rate. Landlords liked variable-rate mortgages because they offer a lower interest rate, compared to fixed rate mortgages. And investors liked them because when rates go up, investors get a higher return, and the market value of the mortgage is largely protected.

But when rates go up a lot, as they have done since March 2022, the interest payments go up a lot, and by late last year, these interest payments began to double, and suddenly the building doesn’t pencil out anymore because rents, especially at office towers that are partially vacant, won’t cover the interest payments.

And then landlords might walk away and lose the equity. And CMBS holders end up with a defaulted mortgage and an office tower whose price at a sale will be far below the loan value. We have discussed the revenge of variable-rate office mortgages here.

CRE Nightmare for CMBS Holders: Office Mortgage Delinquency Rate Has Biggest Six-Month Spike Ever. It’s just the Beginning

by Wolf Richter • Jul 5, 2023 • 132 Comments

And it’s structural. Variable-rate CRE mortgages and much higher rates just speed up the process.

By Wolf Richter for WOLF STREET.

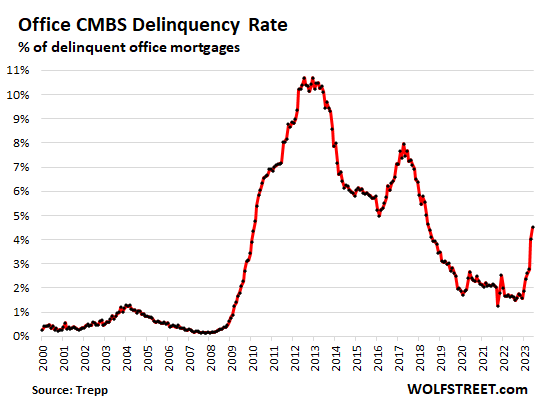

After blowing through the pandemic with no more than a squiggle, the delinquency rate of Commercial Mortgage-Backed Securities (CMBS) backed by office properties jumped to 4.5% by loan balance in June, up from 1.6% just six months ago in December 2022, according to Trepp, which tracks and analyses CMBS.

Office mortgages that had been packaged into CMBS went through a horrendous default cycle following the Financial Crisis, with the delinquency rate topping out at over 10% in 2012/2013.

But this current six-month 2.9-percentage-point spike from 1.6% to 4.5% is the fastest six-month spike in Trepp’s data going back to 2000.

So this is going to be interesting because we’re just at the beginning of a massive structural change – not a temporary blip – that is impacting office towers; turns out, companies have figured out they won’t ever need this vast amount of vacant office space.

Trepp considers a loan “delinquent” after the penalty-free 30-day grace period ends and the borrower still hasn’t caught up with the interest payment.

This delinquency rate does not include properties that are still paying interest but are past due on paying off the mortgage on maturity date. This includes the interest-only mortgages, when the whole amount is due at maturity, and mortgages with a balloon payment at maturity. As long as landlords are making interest payments, Trepp doesn’t consider the mortgages delinquent, but tracks mortgages that are past their maturity date separately.

For example, Trepp’s overall delinquency rate for all types of CMBS rose to 3.90% in June. Including the loans that were past their maturity date but were still paying interest, the delinquency rate would have risen to 4.66%.

CMBS have real advantages. They allow lenders, such as banks, to sell high-risk commercial mortgages during times of low interest rates to yield-chasing investors, such as bond funds, life insurers, etc. For banks, these mortgages might be too risky to keep on their books.

So they package them, sometimes just one big mortgage, but often several or many mortgages, into a pool of mortgages that then gets structured into different slices that investors buy, with the junk-rated slices taking the first losses in return for slightly higher yields. The top-rated slices have an A-rating or AA-rating, solidly investment grade (here’s my cheat sheet on bond credit ratings by rating agency), with the idea that the lowest rated slices will absorb any losses while the top-rated slices remain unscathed.

The mortgages – as we have seen in the current wave of defaults, including those where the landlord has just walked away from the property – are often variable-rate. Landlords liked variable-rate mortgages because they offer a lower interest rate, compared to fixed rate mortgages. And investors liked them because when rates go up, investors get a higher return, and the market value of the mortgage is largely protected.

But when rates go up a lot, as they have done since March 2022, the interest payments go up a lot, and by late last year, these interest payments began to double, and suddenly the building doesn’t pencil out anymore because rents, especially at office towers that are partially vacant, won’t cover the interest payments.

And then landlords might walk away and lose the equity. And CMBS holders end up with a defaulted mortgage and an office tower whose price at a sale will be far below the loan value. We have discussed the revenge of variable-rate office mortgages here.

And so even landlords – giant landlords such as private equity firm Blackstone and private equity firm Brookfield – have defaulted on the mortgages and then walked away from the property. They lose the equity in the property, and the lenders then have to sell the office tower for whatever they can get.

But whatever they can get for older office towers is a lot lot less than anyone had imagined a few years ago when the CMBS were issued. The losses on the mortgages for CMBS holders are huge, such as 88% and 82% by two Class-A office towers in Houston, or even a total loss, with the proceeds of the foreclosure sale just paying for fees and expenses, which happened with the vacant 46-story former One AT&T Center in downtown St. Louis. Two class-A office towers in San Francisco sold at 70% off the pre-pandemic price estimates, though they didn’t involve mortgages. Other office towers were sold with 40% to 50% in losses.

So these older office towers create some serious investor-bloodletting – but it’s thinly spread around the globe, from the bond fund in your portfolio to a pension fund in a foreign country.

And it’s structural, not a market blip; it’s an issue that will have to be dealt with over many years, such as by tearing down office towers or by converting them into residential buildings where possible.

Even lower interest rates won’t make vacant or half-vacant office towers economically viable. Markets, if allowed to do the dirty work, are good at pricing those situations, and providing a low cost-base for developers with an appetite for risk to redevelop those properties, at the expense of existing investors.

fb account for sale account acquisition guaranteed accounts

buy aged facebook ads accounts buy pre-made account profitable account sales

tiktok ad accounts https://tiktok-ads-agency-account.org

tiktok ad accounts https://buy-tiktok-ads.org

buy tiktok ad account https://buy-tiktok-business-account.org

buy tiktok ads account https://buy-tiktok-ads-accounts.org

tiktok agency account for sale https://buy-tiktok-ad-account.org

buy tiktok ads https://tiktok-agency-account-for-sale.org

tiktok agency account for sale https://tiktok-ads-account-for-sale.org

buy tiktok ads https://tiktok-ads-account-buy.org

buy tiktok ads https://buy-tiktok-ads-account.org

buy fb business manager buy-business-manager-accounts.org

buy facebook bm buy business manager account

buy business manager account https://buy-bm.org

fb bussiness manager https://buy-business-manager-verified.org

buy verified business manager facebook https://business-manager-for-sale.org

buy facebook business manager https://buy-verified-business-manager.org

buy facebook verified business account https://buy-verified-business-manager-account.org/

facebook verified business manager for sale buy-bm-account.org

buy business manager facebook https://buy-business-manager-acc.org/

old google ads account for sale https://ads-agency-account-buy.click

buy google ad account https://buy-verified-ads-account.work

buy verified facebook business manager account https://buy-business-manager.org/

buy google adwords accounts buy verified google ads accounts

buy google ads threshold account https://buy-ads-agency-account.top

buy google ads account https://buy-account-ads.work

buy google ads accounts buy adwords account

buy google ads account https://ads-account-buy.work

google ads agency account buy https://ads-account-for-sale.top

buy facebook account https://buy-accounts.click

buy adwords account https://buy-ads-accounts.click

buy old google ads account https://buy-ads-account.top

cheap facebook accounts https://ad-accounts-for-sale.work

buy facebook accounts buy facebook profile

facebook ads account buy buy facebook accounts for advertising

buy facebook account facebook ad account buy

facebook ad account buy buy facebook account

buy facebook advertising accounts https://buy-ads-account.click

buy facebook account for ads https://buy-ad-account.top

buying fb accounts https://buy-ad-accounts.click

facebook ads account buy https://buy-adsaccounts.work

покупка аккаунтов купить аккаунт

купить аккаунт https://akkaunty-dlya-prodazhi.pro

площадка для продажи аккаунтов https://online-akkaunty-magazin.xyz/

биржа аккаунтов https://akkaunty-optom.live

магазин аккаунтов https://kupit-akkaunty-market.xyz/

покупка аккаунтов маркетплейсов аккаунтов

биржа аккаунтов https://akkaunt-magazin.online

площадка для продажи аккаунтов kupit-akkaunt.xyz

продажа аккаунтов rynok-akkauntov.top

маркетплейс аккаунтов соцсетей akkaunty-na-prodazhu.pro

social media account marketplace account market

sell pre-made account https://accounts-marketplace.online

account exchange https://buy-accounts.live

accounts market https://social-accounts-marketplace.live

find accounts for sale https://accounts-marketplace.art

guaranteed accounts https://buy-accounts-shop.pro

profitable account sales accounts marketplace

buy account https://social-accounts-marketplace.xyz

accounts market buy accounts

account exchange service https://social-accounts-marketplaces.live

buy and sell accounts https://buy-best-accounts.org/

website for buying accounts accounts-marketplace.xyz

account trading platform https://accounts-offer.org

social media account marketplace ready-made accounts for sale

purchase ready-made accounts buy and sell accounts

marketplace for ready-made accounts account selling service

find accounts for sale account store

secure account purchasing platform account exchange service

secure account purchasing platform marketplace for ready-made accounts

account store account exchange service

social media account marketplace online account store

sell account account-buy.org

account market account sale

account exchange purchase ready-made accounts

account selling service account market

account store secure account sales

account marketplace account exchange service

guaranteed accounts find accounts for sale

accounts market account trading service

online account store buy and sell accounts

verified accounts for sale accounts-marketplace.org

sell accounts verified accounts for sale

online account store verified accounts for sale

purchase ready-made accounts ready-made accounts for sale

buy account account trading service

buy account sell accounts

buy account https://accountsmarketbest.com

account sale sell accounts

sell accounts account store

profitable account sales accounts marketplace

account purchase account store

Buy Account Secure Account Purchasing Platform

Website for Buying Accounts Find Accounts for Sale

Buy Pre-made Account Purchase Ready-Made Accounts

Account Buying Service socialmediaaccountsshop.com

Buy Account Account Buying Platform

Account Store Account Store

Purchase Ready-Made Accounts Account Selling Platform

Account exchange Account trading platform

Website for Selling Accounts Account Purchase

Buy and Sell Accounts Account Store

Account Buying Service Account Selling Service

маркетплейс аккаунтов соцсетей платформа для покупки аккаунтов

безопасная сделка аккаунтов гарантия при продаже аккаунтов

маркетплейс аккаунтов https://prodat-akkaunt-online.ru/

площадка для продажи аккаунтов безопасная сделка аккаунтов

биржа аккаунтов https://magazin-akkauntov-online.ru/

маркетплейс для реселлеров https://marketplace-akkauntov-top.ru/

покупка аккаунтов магазин аккаунтов

Wow, marvelous blog format! How long have you ever been running a blog for?

you made running a blog look easy. The whole glance of your web site is magnificent,

let alone the content! You can see similar here e-commerce

Oprogramowanie do zdalnego monitorowania telefonu komórkowego może uzyskiwać dane docelowego telefonu komórkowego w czasie rzeczywistym bez wykrycia i może pomóc w monitorowaniu treści rozmowy.