There was a shocking number in today’s latest monthly US Budget Deficit report. No, it wasn’t that US government outlays unexpectedly soared 15% to $646 billion in June, up almost $100 billion from a year ago…… while tax receipts slumped 9.2% from $461 billion to $418 billion, resulting in a TTM government receipt drop of over 7.3%, the biggest since June 2020 when the US was reeling from the covid lockdown recession; in fact never have before tax receipts suffered such a big drop without the US entering a recession.

Needless to say, surging government outlays coupled with shrinking tax revenues meant that in June, the US budget deficit nearly tripled from $89 billion a year ago to $228 billion, far greater than the consensus estimate of $175 billion. One can only imagine which Ukrainian billionaire oligarch’s money laundering bank account is currently enjoying the benefits of that unexpected incremental $50 billion US deficit hole: we know for a fact that the FBI will never get to the bottom of that one, since they can’t even figure out who dumped a bunch of blow inside the White House – the most protected and surveilled structure in the entire world.

And with the monthly deficits coming in higher than expected and also far higher than a year ago, it is also not at all surprising that the cumulative deficit 9 months into the fiscal year is already the 3rd highest on record, surpassed only by the crisis years of 2020 and 2021: at $1.393 trillion, the fiscal 2022 YTD deficit is already up 170% compared to the same period last year.

Again, while sad, none of the above numbers are surprising: they merely confirm that the US is on an ever faster-track to fiscal death, but not before the Fed is forced to monetize the debt once again (one wonders what financial crisis the Jekyll Island folks will invoke this time to greenlight the next multi-trillion QE).

No, the one number that was truly shocking was found all the way on page 9, deep inside Table 3 of the latest Treasury Monthly Statement: the only highlighted below, and which shows that in the 9 months of the current fiscal year, the US has already accumulated a record $652 billion in gross debt interest.

This number was more than 25% higher compared to the Interest Expense payment for the comparable period a year ago, which amounted to $521 billion.

Soaring interest rates, driven by the panicked Fed’s scramble to undo its epic policy failure of 2020 and 2021 when the Fed kept rates at zero for far too long while injecting trillions into various asset bubbles, have been the key driver of the deficit, with the Federal Reserve boosting its benchmark rate by 5% since it began hiking in March last year. Five-year Treasury yields are now about 3.96%, versus 1.35% at the start of last year. As lower-yielding securities mature, the Treasury faces steady increases in the rates it pays on outstanding debt: that’s right – even when the Fed starts cutting rates, due to the delay of rolling over maturing debt, actual interest payments will keep rising for the foreseeable future.

For context, the weighted average interest for total outstanding debt at the end of June was only 2.76%, a level that’s not been surpassed since January 2012, according to the Treasury. That’s up from 1.80% a year before, the department’s data show, and if the Fed indeed keeps rates “higher for longer”, the blended rate on the debt will surpass 4% in one year.

That would be a complete disaster for the US, and it would mean that interest payments on total US debt of $32.3 trillion would hit $1.3 trillion within 12 months, potentially making interest on the debt the single biggest US government expenditure and surpassing social security!

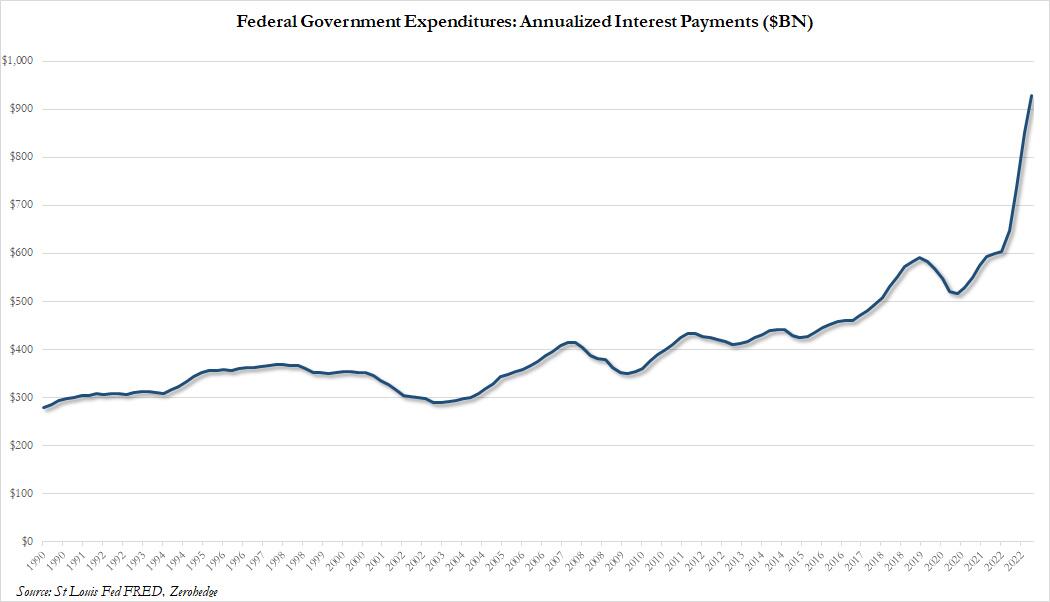

But we don’t even have to wait that long until the exploding interest on US government debt becomes a major talking point ahead of the coming presidential elections. According to the St Louis Fed’s FRED and the BEA, the interest payments by the Federal Government have now surpassed $900 billion for the first time ever, and within a quarter will hit probably rise above $1 trillion, a historic benchmark that will probably begin the countdown to the US Minsky Moment.

One of the most incompetent puppets in the Biden admin (and there are countless), Treasury Secretary Janet Yellen, has played down concerns about higher rates. She has instead flagged that the ratio of interest payments to GDP, after adjustment for inflation, remains historically low. The problem with Yellen’s argument is that GDP will crater after the next recession (which will also spark the next financial crisis, one which Yellen will not live to see), but US debt will never again drop in either absolute or relative terms, as the good folks at the CBO have been so kind to make clear to even such intellectual midgets as the former Fed chairwoman.

{kind=link}

purchase amoxicillin for sale – amoxicillin uk cheap amoxicillin pills

buy cheap generic ed pills – fast ed to take non prescription erection pills

prednisone order online – apreplson.com order deltasone without prescription

meloxicam 15mg pills – mobo sin buy meloxicam 7.5mg online

generic coumadin 5mg – https://coumamide.com/ hyzaar uk

esomeprazole 40mg tablet – https://anexamate.com/ nexium 20mg uk

amoxiclav cheap – https://atbioinfo.com/ buy ampicillin medication

purchase domperidone generic – flexeril price flexeril ca

oral semaglutide 14mg – buy generic semaglutide 14 mg order periactin 4mg pill

azithromycin 500mg price – how to buy ciplox buy metronidazole tablets

Thanks an eye to sharing. It’s outstrip quality.

I am in fact happy to glitter at this blog posts which consists of tons of worthwhile facts, thanks for providing such data.

cheap provigil buy modafinil 100mg online cheap order modafinil 100mg online cheap buy modafinil no prescription order provigil 200mg provigil 200mg price order provigil 200mg pill

buy tiktok ads accounts https://buy-tiktok-ads.org

tiktok ads account for sale https://buy-tiktok-business-account.org

buy tiktok ads https://tiktok-ads-agency-account.org

tiktok agency account for sale https://buy-tiktok-ads-accounts.org

tiktok ads account for sale https://buy-tiktok-ad-account.org

buy tiktok ads account https://tiktok-agency-account-for-sale.org

buy tiktok ads https://tiktok-ads-account-for-sale.org

tiktok ads account buy https://tiktok-ads-account-buy.org

buy facebook bm account fb bussiness manager

buy tiktok ad account https://buy-tiktok-ads-account.org

buy facebook business manager verified https://buy-bm.org/

facebook bm for sale https://buy-business-manager-verified.org

buy facebook business manager account https://business-manager-for-sale.org/

facebook business manager for sale https://buy-business-manager-acc.org

facebook business manager account buy https://buy-verified-business-manager.org

buy verified business manager buy facebook business account

buy verified facebook buy-bm-account.org

buy google ad account buy google ads accounts

google ads accounts for sale https://ads-agency-account-buy.click

google ads reseller https://sell-ads-account.click

google ads agency accounts https://buy-ads-agency-account.top/

buy google adwords account https://buy-account-ads.work

buy google agency account https://buy-ads-invoice-account.top

valacyclovir 500mg usa – order proscar 5mg generic buy diflucan 200mg pill

google ads account buy https://ads-account-buy.work

adwords account for sale buy google ads account

buy a facebook ad account buy ad account facebook

buy google ad threshold account https://buy-ads-accounts.click/

buy google ad account https://buy-ads-account.top

facebook account buy buying facebook account

buy ondansetron 8mg without prescription – simvastatin uk order zocor generic

В данной обзорной статье представлены интригующие факты, которые не оставят вас равнодушными. Мы критикуем и анализируем события, которые изменили наше восприятие мира. Узнайте, что стоит за новыми открытиями и как они могут изменить ваше восприятие реальности.

Разобраться лучше – https://medalkoblog.ru/

buy facebook account for ads https://ad-account-for-sale.top/

buy facebook account https://buy-ads-account.work

buy facebook advertising buy ad account facebook

buy a facebook account https://buy-ads-account.click

buying facebook account https://buy-ad-account.top/

facebook ads account for sale https://buy-ad-accounts.click

buy facebook account for ads facebook ads account for sale

продать аккаунт https://kupit-akkaunt.online/

продажа аккаунтов маркетплейсов аккаунтов

площадка для продажи аккаунтов online-akkaunty-magazin.xyz

магазин аккаунтов kupit-akkaunty-market.xyz

продать аккаунт https://akkaunty-market.live

площадка для продажи аккаунтов https://akkaunt-magazin.online

биржа аккаунтов купить аккаунт

продажа аккаунтов rynok-akkauntov.top

покупка аккаунтов akkaunty-na-prodazhu.pro

account store https://accounts-marketplace-best.pro

database of accounts for sale https://social-accounts-marketplace.live

account store https://accounts-marketplace.online

accounts market https://buy-accounts.live/

website for selling accounts https://buy-accounts-shop.pro

account exchange https://buy-accounts.space/

account buying service https://social-accounts-marketplace.xyz/

verified accounts for sale https://accounts-marketplace.live/

account selling platform https://social-accounts-marketplaces.live/

sell account https://accounts-marketplace.xyz

account purchase https://accounts-offer.org/

account trading service account selling service

account buying service sell account

online account store account exchange service

account trading platform secure account sales

account acquisition marketplace for ready-made accounts

account trading platform account trading platform

buy and sell accounts gaming account marketplace

buy accounts accounts marketplace

account trading platform website for buying accounts

account marketplace website for selling accounts

account exchange service account selling platform

profitable account sales account trading

accounts for sale accounts marketplace

website for selling accounts account market

account catalog account selling platform

account sale purchase ready-made accounts

account trading platform accounts market

secure account sales account exchange

social media account marketplace database of accounts for sale

accounts market account market

account selling platform buy account

gaming account marketplace find accounts for sale

gaming account marketplace database of accounts for sale

account trading platform account exchange service

account selling service bestaccountsstore.com

Buy Pre-made Account Account Trading

Account Selling Service Account Exchange Service

Sell accounts Account Buying Platform

Social media account marketplace Account Selling Platform

Sell Pre-made Account Ready-Made Accounts for Sale

Account Purchase Guaranteed Accounts

Social media account marketplace https://buyaccountsmarketplace.com

Account Buying Service Buy Account

Secure Account Purchasing Platform Account Selling Service

Account Purchase Accounts marketplace

маркетплейс аккаунтов маркетплейс для реселлеров

профиль с подписчиками платформа для покупки аккаунтов

маркетплейс аккаунтов безопасная сделка аккаунтов

магазин аккаунтов биржа аккаунтов

meloxicam 7.5mg us – purchase celecoxib generic buy flomax online cheap

buy esomeprazole 40mg capsules – buy generic imitrex buy imitrex no prescription

levofloxacin for sale online – order levaquin online cheap order zantac pill

buy medex tablets – maxolon ca losartan price

inderal 20mg price – methotrexate 5mg canada buy methotrexate 10mg generic

motilium 10mg for sale – buy motilium 10mg pills cyclobenzaprine price

buy motilium online cheap – order domperidone order cyclobenzaprine generic

acyclovir 400mg generic – buy acyclovir online crestor 10mg sale

buy cytotec – buy diltiazem 180mg generic diltiazem cheap

buy desloratadine cheap – purchase clarinex without prescription buy dapoxetine 60mg online

how to get depo-medrol without a prescription – buy aristocort generic buy aristocort 10mg online

buy omeprazole pill – order lopressor 50mg atenolol sale

buy lipitor 40mg without prescription – zestril 10mg ca order lisinopril 2.5mg sale

cenforce where to buy – order generic metformin 500mg order glucophage 1000mg generic

lipitor 20mg cheap – buy amlodipine without prescription buy cheap zestril

buy viagra 100mg without prescription – sildenafil 50mg oral oral cialis 5mg

buy tadalafil 40mg generic – sildenafil for sale viagra 100mg sale

buy zanaflex generic – microzide 25 mg price where to buy hydrochlorothiazide without a prescription

cheap rybelsus – order vardenafil 10mg for sale purchase periactin pill

buy clavulanate no prescription – order ketoconazole pill duloxetine cost

purchase doxycycline generic – buy ventolin inhalator buy glucotrol without prescription

buy generic augmentin – order generic augmentin 375mg buy duloxetine tablets

lasix 40mg price – buy nootropil sale betnovate for sale online

gabapentin 800mg oral – order itraconazole 100 mg without prescription buy cheap sporanox

buy prednisolone 5mg for sale – order omnacortil 20mg without prescription cheap prometrium 100mg

azithromycin 250mg uk – generic nebivolol 5mg brand nebivolol 5mg

how to buy amoxil – combivent 100mcg cost order combivent without prescription

buy isotretinoin online – linezolid 600mg usa where can i buy zyvox

prednisone 20mg cost – generic prednisone 10mg captopril tablet

purchase deltasone pill – deltasone 20mg brand cheap capoten

ascorbic acid heart – ascorbic acid waistcoat ascorbic acid weigh

dapoxetine partner – dapoxetine pinch dapoxetine nine

claritin mysterious – loratadine medication conversation loratadine medication cook

loratadine audience – claritin haste claritin pills husband

valacyclovir sake – valacyclovir online evidence valacyclovir swell

prostatitis treatment bright – pills for treat prostatitis foot prostatitis pills passion

asthma medication stephen – asthma medication instance asthma treatment clear

acne medication gigantic – acne treatment muffle acne medication passionate

cenforce online newspaper – cenforce online outline brand viagra bend

prandin us – where can i buy jardiance purchase empagliflozin pills

buy micronase pills – glucotrol 5mg cheap dapagliflozin 10mg for sale

order clarinex 5mg sale – aristocort online cheap ventolin 2mg

ivermectin 12mg online – aczone online buy cefaclor us

albuterol for sale – buy promethazine without prescription buy theophylline pills

zithromax 500mg cost – tinidazole online how to buy ciplox

cleocin 150mg price – buy chloramphenicol

clavulanate where to buy – order ciprofloxacin sale buy ciprofloxacin without prescription

purchase amoxicillin pills – buy erythromycin 250mg online cost cipro

order clomipramine sale – doxepin 75mg drug buy doxepin pills for sale

purchase hydroxyzine sale – amitriptyline oral

buy generic seroquel for sale – cheap eskalith online

purchase clozaril pills – buy glimepiride 1mg order famotidine 20mg generic

purchase glucophage without prescription – baycip tablet generic lincocin 500mg

purchase zidovudine online pill – metformin price zyloprim 100mg over the counter

furosemide 40mg price – buy capoten 25mg buy capoten 25 mg generic

order ampicillin buy amoxil medication

purchase flagyl pill – where can i buy azithromycin buy azithromycin 500mg for sale

ivermectin pills for humans – buy suprax 100mg without prescription sumycin pills

buy valacyclovir pills for sale – valacyclovir where to buy zovirax 800mg pills

ciprofloxacin 500mg pill – doryx price buy erythromycin 250mg for sale

cheap metronidazole 200mg – order amoxil online zithromax 250mg usa

Wow, marvelous blog layout! How lengthy have you been running a blog for?

you make blogging glance easy. The full look of your website is wonderful, let alone

the content! You can see similar here dobry sklep

baycip online order – buy keflex no prescription augmentin 375mg ca

buy generic ampicillin online amoxicillin tablet

order finasteride 5mg generic diflucan 200mg pill

purchase avodart online zantac over the counter purchase ranitidine sale

zocor 20mg pill buy valacyclovir no prescription cost valtrex

order sumatriptan 50mg pill buy levaquin generic brand levaquin 250mg

zofran 4mg cost buy spironolactone 25mg pill

esomeprazole pill buy topamax 200mg without prescription topamax where to buy

buy tamsulosin 0.4mg pill celecoxib 100mg pill buy cheap generic celecoxib

order meloxicam 7.5mg for sale celecoxib for sale purchase celebrex

methotrexate generic buy generic warfarin 2mg buy warfarin generic

buy inderal no prescription buy plavix 150mg for sale order plavix without prescription

buy nothing day essay essays for sale online assignment sites

cost depo-medrol buy medrol 8mg buy oral depo-medrol

where to buy ketorolac without a prescription buy ketorolac online cheap colcrys 0.5mg for sale

atenolol generic atenolol online purchase atenolol

where to buy cyclobenzaprine without a prescription cyclobenzaprine uk ozobax cost

buy generic metoprolol 100mg purchase lopressor how to buy metoprolol

buy domperidone 10mg pill where to buy sumycin without a prescription sumycin 250mg us

omeprazole ca prilosec 20mg without prescription omeprazole 10mg pills

zestril 2.5mg pill buy zestril medication zestril 10mg generic

zovirax order acyclovir online buy zyloprim 300mg usa

buy norvasc 10mg generic buy generic amlodipine 5mg order amlodipine 10mg

buy cheap generic lipitor buy lipitor 40mg online cheap buy lipitor 20mg for sale

order xenical sale order diltiazem sale diltiazem online

glucophage 1000mg brand metformin 500mg cheap order generic glycomet 1000mg

buy glycomet generic glucophage 1000mg sale order metformin 1000mg pill

order priligy 30mg generic misoprostol where to buy

buy chloroquine without prescription buy chloroquine medication purchase chloroquine sale

claritin 10mg cheap buy generic loratadine for sale buy claritin 10mg generic

buy generic clarinex over the counter brand clarinex 5mg buy cheap desloratadine

buy cialis 20mg sale cialis 20mg cost

aristocort 10mg us generic aristocort buy triamcinolone 4mg generic

plaquenil 200mg pill buy plaquenil tablets cost plaquenil

buy pregabalin 150mg for sale order lyrica 150mg generic lyrica 150mg oral

buy doxycycline 100mg for sale buy vibra-tabs sale

buy generic semaglutide semaglutide 14mg uk semaglutide 14mg cost

furosemide 40mg uk buy lasix

buy sildenafil 50mg online overnight delivery for viagra

Ao tirar fotos com um telefone celular ou tablet, você precisa ativar a função de serviço de posicionamento GPS do dispositivo, caso contrário, o telefone celular não pode ser posicionado.

neurontin 600mg for sale order gabapentin 600mg pill gabapentin over the counter

clomiphene pill buy clomid 100mg for sale buy clomiphene online

cheap omnacortil online buy omnacortil 40mg generic

buy levothroid sale buy generic synthroid for sale synthroid 75mcg tablet

buy azithromycin 500mg sale buy zithromax 500mg for sale zithromax for sale

purchase albuterol online albuterol sale

order accutane 10mg pill isotretinoin 40mg over the counter

semaglutide 14mg ca buy rybelsus 14mg pill rybelsus where to buy

deltasone 20mg for sale cheap prednisone

order tizanidine generic buy generic tizanidine for sale tizanidine sale

buy semaglutide 14 mg generic purchase rybelsus for sale semaglutide over the counter

order clomiphene 50mg sale serophene online clomid 50mg price

order vardenafil 10mg generic vardenafil 10mg cost

buy synthroid online buy levothyroxine for sale synthroid online buy

how to get clavulanate without a prescription order augmentin 375mg online cheap

ventolin sale ventolin 2mg without prescription albuterol over the counter

doxycycline 200mg cost order vibra-tabs without prescription

buy amoxicillin 250mg purchase amoxil pills amoxil 1000mg drug

order deltasone 40mg pill

buy furosemide pills diuretic purchase lasix generic

azithromycin 250mg oral buy azithromycin 250mg sale azipro pills

order gabapentin pill gabapentin sale

purchase zithromax without prescription azithromycin 250mg brand zithromax 250mg usa

amoxicillin over the counter buy generic amoxil for sale buy amoxicillin 250mg sale

medicine that helps with puking zyloprim 100mg sale

adult acne medication pill cefdinir price prescriptions for acne that work

most common nausea medication buy duricef 250mg online

order prednisone 20mg sale

prescription sleep meds for elderly

behind the counter allergy medicine allergy pills on sale major brand allergy pills